Welcome to this week’s Market Pulse, your 5 minute update on key market news and events, with takeaways and insights from the Sidekick Investment Team.

Our stories this week are:

- Unexpected Magnificents

- Economic Surprises

- Gemini Woes

It’s important to note that the content of this Market Pulse is based on current public information which we consider to be reliable and accurate. It represents Sidekick’s view only and does not represent investment advice - investors should not take decisions to trade based on this information.

1) Unexpected Magnificents

From the Nifty Fifty [1], the GRANOLAS[2], the FAANGs[3], the BRICSs [4]... and, of course, the Magnificent Seven [5] - market participants love to describe their favourites with creative names and acronyms. But what about the Magnificent 8 - Europe's top 8 aerospace and defence companies? You haven't heard of them, or if you did, you probably wouldn't put them anywhere near the word "magnificent".

Indeed, for most of the last two decades, Europe's aerospace and defence companies have been anything but magnificent. The politically sensitive sector driven by government spending, the lumpy nature of projects and complicated accounting have made the industry a minefield [6] for investors [7]. The rise of ESG (Environmental, Social and Governance) investing has yet to help either, with exclusionary screening strategies often making the sector uninvestable [8]. As a result, the sector underperformed the broader European market by more than 125% during 2005-2022 [9].

Fast forward two years, and the word "magnificent" takes on new resonance. This Saturday marked the second anniversary of Russia's invasion of Ukraine, sparking the most consequential conflict in Europe since WWII. The aerospace and defence sector has surged by over 140% during this period. Shares of companies such as Rheinmetall, Saab, and Leonardo have witnessed a three to fourfold increase. At the same time, BAE Systems has more than doubled. While war is never a cause for celebration, irrespective of which side you're on, it positions the industry at the forefront of European policymakers' attention.

In response to the conflict, European nations are rethinking the importance of defence investments. The increased budgets aren't just a reaction to the current war in Ukraine. They are essential to addressing years of inadequate investment and building a robust defence against the ongoing threat posed by Russia in Europe.

This year's fundamental question is the impact of a potentially isolationist US on European defence. There are plenty of challenges, from Trump's recent NATO comments [10] to Republican opposition blocking $60 billion in military aid to Ukraine. But despite internal opposition, the EU's recent €50bn financial aid agreement for Ukraine [11] and bilateral military commitments from Germany, France, and the UK may boost defence budgets.

Still, they can't fully replace the US military contribution [12]. Strong support for the European defence industry is thus expected to persist regardless of this year's US election outcome.

2) Economic Surprises: What really moves the markets

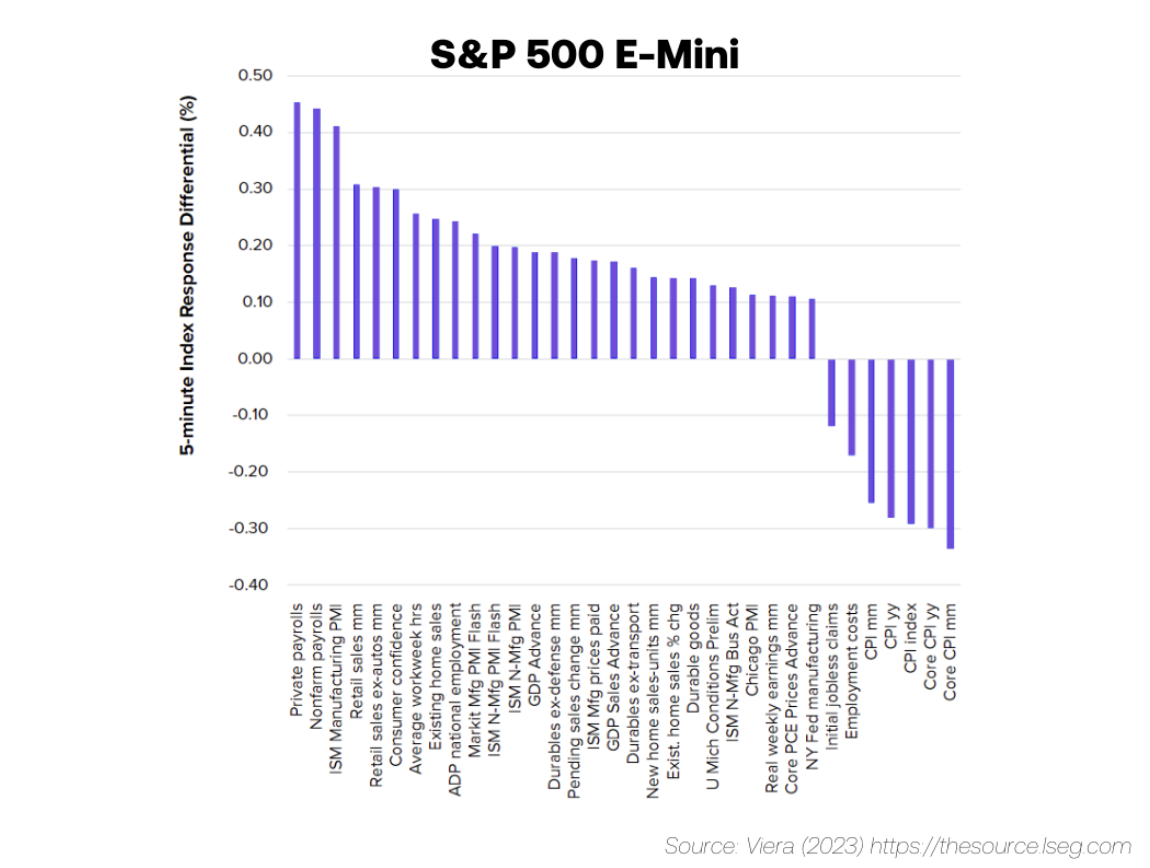

This week was a data-heavy one with an abundance of economic releases from Global manufacturing PMIs to US core PCE and GDP readings, to name a few. Which ones mattered the most?

Maria Viera from the London Stock Exchange Group has studied the impact of economic surprises in the US equity market by looking at market movements in the 5-minute interval after a data release and measured the average difference in performance between the 20% largest and 20% smallest surprises [13].

The S&P 500 shows notable reactions to unemployment data, core inflation, manufacturing PMI, retail sales, and consumer confidence. This is because unemployment data reflects economic growth strength and influences future monetary policy. Meanwhile, manufacturing PMI and consumer confidence serve as forward-looking indicators, offering insights into future GDP growth.

The study comes with a caveat: it was conducted from 2009 to 2022, a period mainly characterised by zero interest rates. Nevertheless, it underscores the value of concentrating on the most impactful data points when dealing with abundant information and limited time.

3) Gemini Woes

Alphabet witnessed a roughly -5% decline this week due to numerous instances of bias in Gemini's generated results, in images and text. Consequently, Alphabet withdrew the Gemini image generator and issued an apology [14]. The stock continues to get penalised for poor product launches or competitor product announcements, highlighting the narrative risk around Google as a Gen AI loser.

If competition is a risk to Google Search, we don't see it in any data. ChatGPT's engagement growth is plateauing, and Bing has been losing search revenue share since Microsoft declared war a year ago[15].

The current Gen AI offerings have yet to prove a compelling alternative to Google Search. There's no doubt about the increased utility of Gen AI applications to create text, images and code. Still, for consumers to permanently change behaviour beyond the novelty of a new product, they need trust, speed and choice - which are critical for most revenue generating search queries.

While we don't underestimate Alphabet's challenges, we believe that as Gen AI answers earn consumers' trust, Google is well-positioned to seamlessly integrate these responses with web query results, providing users with an optimal experience that combines the strengths of both search and Gen AI.

A year and a half ago, Alphabet was the "set and forget" stock you wouldn't have to worry about. On the other hand, Meta was facing an existential crisis centred around Zuckerberg's reckless spending on the Metaverse; the "nobody uses Facebook anymore" argument and their ad business being permanently impaired by Apple. Fast forward to today, and Meta has completely turned around the narrative, delivering 4x returns in the process.

Today, it is Alphabet that's in the tough spot. It's up to them to prove the naysayers wrong.

Note: We own Alphabet, Meta and Apple in our Flagship Strategy

References

[1] The "Nifty Fifty" were a set of high-performing blue-chip stocks, including companies like IBM and Coca-Cola, during the 1960s and 1970s.

[2] https://edition.cnn.com/2024/02/27/investing/granolas-europe-stocks-magnificent-7/index.html

[3] The FAANGs refer to a group of high-performing technology stocks: Facebook (now Meta), Apple, Amazon, Netflix, and Google parent company Alphabet.

[4] BRICs refer to a group of four major emerging national economies: Brazil, Russia, India, and China, characterised by significant growth potential and influence on regional and global affairs.

[5] The term 'Magnificent 7' draws inspiration from the iconic Western film of the same name, and is now used to describe a group of highly influential tech giants (Apple, Microsoft, Alphabet, Amazon, Tesla, Meta, Nvidia) that dominate the US stock market.

[6] No pun intended

[7] Bloomberg, GS

[8] https://www.ft.com/content/e14ea515-a6f3-4763-9def-7bc40d3b2e4a

[9] As measured by Goldman Sachs basket of European Defense stocks (GSSBDEFE Index) vs the Stoxx 600 Europe.

[10] https://edition.cnn.com/2024/02/10/politics/trump-russia-nato/index.html

[12] https://www.ifw-kiel.de/topics/war-against-ukraine/ukraine-support-tracker/

[13] https://thesource.lseg.com/thesource/getfile/index/0cc44f07-63dc-456f-89cc-003ea8edab44

[14] https://blog.google/products/gemini/gemini-image-generation-issue/

[15] https://gs.statcounter.com/search-engine-market-share#monthly-200901-202303%22%3EStatCounter

Notices

Please remember, investing should be viewed as longer term. Your capital is at risk — the value of investments can go up and down, and you may get back less than you put in.