Welcome to this week’s Market Pulse, your 5-minute update on key market news and events, with takeaways and insights from the Sidekick Investment Team.

Our three stories this week:

- Stock Picking Season

- Consumer Conundrum

- Greedflation and Corporate Profits

Adrian (Portfolio Manager), and the rest of the Sidekick team.

It’s important to note that the content of this Market Pulse is based on current public information which we consider to be reliable and accurate. It represents Sidekick’s view only and does not represent investment advice - investors should not take decisions to trade based on this information.

1) Stock Picking Season

This earnings season has been near perfect. First-quarter earnings, now published by 85% plus of the S&P 500’s members, put the index’s profits on course for their strongest growth since the second quarter of 2022, when higher inflation and higher rates began to take effect. Similarly, more than 60% of the Stoxx 600 companies have reported in Europe, with the aggregate positive earnings surprise nearing 8% [1].

But while tech earnings are coming in strong – with the notable exception of Meta which suffered setbacks this quarter – underneath the surface this earnings season has been marked by increased volatility and a return of stock dispersion.

Dispersion means that even though the overall market is doing well, individual stocks are moving with unusual independence from each other.

The evidence? Q1 24 was the best first quarter for equity long-short alpha since 2010 when the data began according to Morgan Stanley [2]. Notably, the alpha generation is coming from both long and short positions, across all three major regions: the US, Europe, and Asia.

The dynamic is largely driven by the Federal Reserve's changing stance on interest rates. At the beginning of the year, the market anticipated eight interest rate cuts from the Fed. Current expectations have shifted, with only one cut now anticipated.

While headlines may scream about the dominance of macroeconomics, a closer look at year-to-date performance and alpha generation reveals a surprisingly micro-driven market. This presents a unique opportunity for active investors: to capitalise on these micro trends within a relatively low-volatility environment.

2) Consumer Conundrum

While earnings reports have been generally positive overall, comments from CEOs about the state of the economy have us revisiting a closely watched area of the market: the US consumer.

Several companies have raised red flags in Q1 with Starbucks seeing the most dramatic stock price reaction – a 15% decline on the day of the report last week. Starbucks CEO Laxman Narasimhan attributed the miss to a “more cautious consumer, particularly their more occasional customer.” [3] His comments were echoed by the CEOs of Mcdonald's and Domino’s who cautioned that in the current environment customers “want value.”

It’s not just quick-serve restaurants. Despite Amazon’s positive share price reaction on the day of its release - driven by their cloud business – their CEO cautioned that on the retail side, “customers are shopping but remain cautious, trading down on price when they can, and seeking out deals” [3].

JP Morgan CEO Jaime Dimon cautioned in November that the excess savings amassed by low-income consumers are now gone [4]. The strength in financial markets and the persistence of higher for longer interest rates have benefited middle and upper-class consumers who have savings and participate in the market. Meanwhile, the lower income bracket is feeling more pain from the higher interest rates.

Retail and restaurants, where consumers often cut back first, could be early indicators of trouble. In this context, Walmart's results next week hold as much weight as those of tech giant Nvidia.

Note: We own Amazon in our Flagship Strategy.

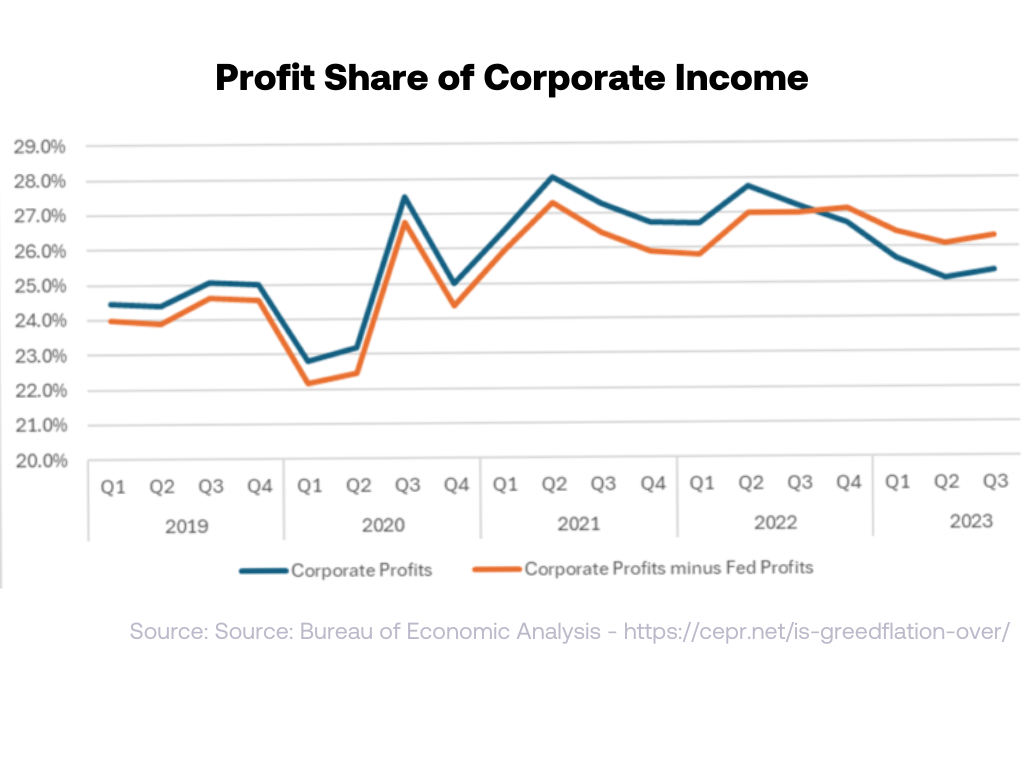

3) Greedflation and corporate profits

One of the reasons earnings have been better than expected so far in Q1 is that profit margins continue to hold up in a post-pandemic world even as supply chains normalise.

By some accounts [5], corporate profits stood at 26.3% of income at the end of last year compared to 24.6% at the end of 2019. This implies that corporations are still pocketing more than 60% of their pandemic dividend:

But while seeking to maximise profits is nothing new for corporate America, in an election year that has inflation at its heart Joe Biden is on a roll. From the famous shrinkflation Super Bowl ad to capping insulin prices and credit card late fees, Biden is obsessed with high prices [6].

And he has good reasons. In a survey conducted between January 2022 and January 2024, the share of US citizens who said “corporations being greedy and raising prices to make record profits” was a major cause of inflation rose to 59% from 44% [7].

The end of the supply chain issues has two effects on corporate margins according to Goldman Sachs: companies can no longer charge a premium for scarce goods but the cost of inputs including labour has become cheaper, offsetting the first effect.

The extent to which corporations can hold on to the recent price hikes remains to be seen. One of our key criteria for selecting stocks for Flagship is pricing power. This year, however, we are keeping a close eye on Mr. Biden too.

References

[1] Bloomberg Finance LP

[5] https://cepr.net/is-greedflation-over/

[6] https://www.nytimes.com/2024/03/06/opinion/biden-inflation-greed-profits.html

[7] https://navigatorresearch.org/wp-content/uploads/2024/02/Navigator-Update-02.14.2024.pdf

Notices

Please remember, investing should be viewed as longer term. Your capital is at risk — the value of investments can go up and down, and you may get back less than you put in.