Welcome to this week’s Market Pulse, your 5-minute update on key market news and events, with takeaways and insights from the Sidekick Investment Team.

Our three stories this week:

- AI’s Secret Power

- Copper is the new Gold

- NBA battle

Adrian (Portfolio Manager), and the rest of the Sidekick team.

It’s important to note that the content of this Market Pulse is based on current public information which we consider to be reliable and accurate. It represents Sidekick’s view only and does not represent investment advice - investors should not take decisions to trade based on this information.

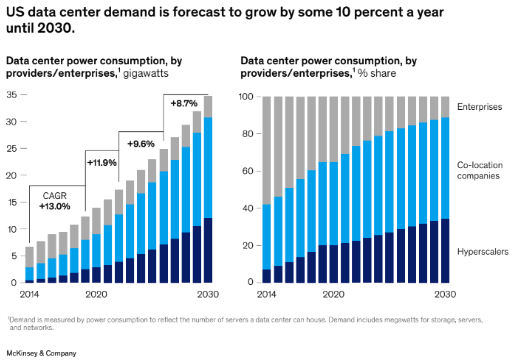

1) AI’s Secret Power

Fueled by skyrocketing AI adoption, investors (including ourselves) are scrambling to identify the next big beneficiaries beyond the usual tech giants like Nvidia, Microsoft, Meta, and Alphabet. While the focus often falls on AI "infrastructure" companies - those involved in chipmaking, cloud services, and data centres - a surprisingly boring sector might also stand to gain: utilities.

The reason? AI's immense power hunger. A hyperscaler’s data centre can use as much power as 80,000 households [1]. Therefore, developing and running these complex algorithms requires vast amounts of energy, making utilities a crucial but often overlooked player in the AI revolution.

The S&P 500 Utilities sector suffered in 2023, declining 10% – its worst performance since 2008. This paled in comparison to the index's overall 24% surge. The reason? Traditionally, utilities struggle during periods of high-interest rates, as was the case in 2023.

The sector has recovered slightly since - it’s up 5.9% year-to-date - but the biggest change in sentiment could come as demand from the new power-hungry centres requires more energy for their AI expansion.

Data centre development is migrating beyond its traditional hubs in Northern Virginia and the Pacific Northwest. Speed to market and readily available power capacity are now the main drivers for new facilities. Industry experts are seeing a surge in data centre demand in Atlanta, San Antonio, Reno, Salt Lake City, and South Carolina. These markets offer competitive commercial and industrial (C&I) electricity rates - and excess power generation compared to established locations.

Utilities positioned to serve these new energy-guzzling regions could see their fortunes dramatically reversed. As the AI revolution unfolds, the most strategically located ones stand to become crucial partners in the digital age. And so, a boring corner of the market could stage an exciting comeback.

2) Copper is the new Gold

Last week, BHP proposed a £31 billion deal to buy Anglo American, one of its largest competitors, in a deal that would mark the mining sector’s biggest on record [3].

Anglo promptly rebuffed the proposal on Friday [4], saying it “significantly undervalues” the company. Nevertheless, there are obvious reasons for BHP’s pursuit, namely its rival’s prized copper mines.

Copper is used almost everywhere in the economy, so is tied to GDP growth. It also benefits from the energy transition with demand from electric vehicles (EVs), electrical grid improvements, and renewables. EVs require a lot more copper than non-electric vehicles — Bernstein (a broker) forecasts EV demand rising from 1 Mt today, to 9 Mt by 2040.

Beyond EV uses, nearly three-quarters of copper consumption goes toward wires; another, half is used in industrial machinery and electrical networks. This widespread application positions copper to benefit tremendously from the underinvestment in renewable energy infrastructure observed in both developed and developing nations. As infrastructure spending ramps up to meet sustainability goals, copper demand is poised to rise due to its crucial role in these projects.

Several factors are converging to create a challenging supply environment for copper. Geologically, copper is a scarce resource, and the quality of existing copper ore deposits naturally deteriorates over time. Furthermore, discoveries of high-grade copper are becoming increasingly rare, leading to a dearth of new mines coming online. While copper recycling plays a significant role, accounting for 30% of global consumption, it cannot fully compensate for the shortfall in mined copper.

To exacerbate these challenges, the highest-grade copper deposits are often located in regions with high geopolitical risk. Additionally, there are no imminent technological breakthroughs expected to revolutionise copper production. These factors collectively create a perfect storm that is likely to constrain copper supply in the face of rising demand.

The rising demand and peaking supply result in an unbalanced market, with a supply deficit opening up after 2027 according to Bernstein. In reality, there’s no such thing as a supply/demand imbalance - just rising copper prices.

With permitting becoming increasingly challenging, greenfield copper mines now take 15 years to reach production which is why BHP – flush with cash from a cyclical boom – would rather buy those assets instead of “building” them. The saga is yet to be over but we would be surprised if Anglo American remains independent by the end of the year.

Note: We own Rio Tinto our Flagship Strategy.

3) An NBA Battle

We wrote about big tech’s increasing interest in live sports in a previous Market Pulse [6] when Netflix acquired the rights to WWE. NFL, MLS and Formula One rights have long been in play but the battle is now moving to the NBA.

Tech giants Amazon (through Prime Video) and Alphabet (through YouTube) are reportedly trying to win the rights from current broadcasters Disney (ESPN) and Warner Bros [5].

Right now, ESPN and Warner Bros. pay a combined $2.8 billion annually to air around 165 games [5]. It’s no surprise that with declining TV viewership, traditional media is struggling to keep live sports. Interestingly, in negotiations for a new contract, both companies seem willing to pay more, but for fewer games.

Why are tech companies interested? The obvious answer is that live sports like the NBA attract viewers who want exclusive content, and advertisers who want to reach those viewers. But the fight goes beyond just games as these tech companies could shape how we experience basketball, or other sports in the future.

Note: We own Amazon and Alphabet in our Flagship Strategy.

References

[2] https://www.spglobal.com/spdji/en/indices/equity/sp-500-utilities-sector/#overview

[3] https://www.ft.com/content/9141eee7-825a-41d7-913d-49e8c12e76db

Notices

Please remember, investing should be viewed as longer term. Your capital is at risk — the value of investments can go up and down, and you may get back less than you put in.