Welcome to this week’s Market Pulse, your 5-minute update on key market news and events, with takeaways and insights from the Sidekick Investment Team.

Our three stories this week:

- Investing at all-time highs

- Demographics and Markets

- Netflix goes Raw

It’s important to note that the content of this Market Pulse is based on current public information which we consider to be reliable and accurate. It represents Sidekick’s view only and does not represent investment advice - investors should not take decisions to trade based on this information.

1) Investing at all-time highs

Last Friday, the S&P 500, the widely-tracked index that reflects over half of the total value of global stock markets, reached a new record high. This marked its first record high since January 3, 2022, and arguably brought a two-year bear market to an end [1].

With interest rates far higher than when the last peak [2], inflation well above target by many measures and a bond market that predicts an almost inevitable recession [3]; you’d be forgiven for raising your eyebrows.

While the Magnificent Seven tech megacaps have been the driving force behind the rally, it's worth noting that the S&P500 Equal-Weight, where each of the 500 members carries an equal weighting, is also hovering near its all-time high [4]. This should help dispel concerns about the market being overly narrow and concentrated.

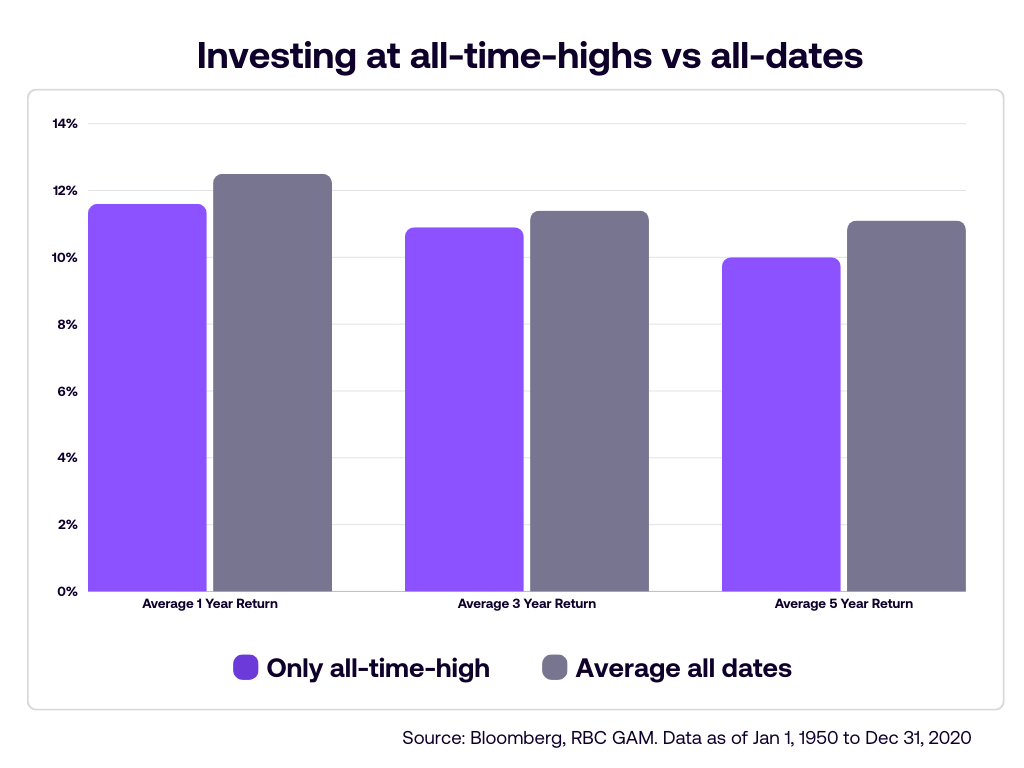

In times like these, investors may face what's known as 'psychological barriers to entry.' They start questioning if it's the right moment to invest new money in the market. The concern arises from the fact that investing at all-time highs means paying a price that's never been paid before, potentially leading to regrets down the road.

But timing the market is almost impossible to get right. And as the charts below show, all-time highs are not uncommon. While caution is essential, completely avoiding them could mean forgoing numerous opportunities.

2) Demographics and Markets

The process of demographic change is so slow that it will have no effect on any market prices this week or next. With so much noise in the World, it’s the type of economic indicator that is easily overlooked. However, research from the Fed suggests that the World’s shifting demographics have played a significant role in economic growth between 1980 and 2016, exceeding that of fiscal or monetary policy, technology, or other productivity-related changes [5].

While the decline in birth rates in developed countries is a familiar topic, the COVID-19 pandemic heightened concerns about a further drop. The recently released 2023 numbers appear to validate those worries:

To some extent, this is not surprising. The pandemic shifted priorities, possibly leading many couples to delay having children. While this may be a temporary Covid-related dip, there are signs of a more prolonged decline. Economic factors, like the affordability of housing and rising education costs, play a role in a delay in starting a family. This contributes to the ongoing trend of starting families later, which began with more women entering the workforce and shows no signs of reversing:

The economic implications are immense, although economists still debate how it will play out. Researchers at the Fed believe that as the COVID-19 impact recedes, the US economy will return to a new normal of low investment, low-interest rates and low output growth [5].

Others believe we are at a turning point where the total size of the working-age population of the developed world, relative to the retired population, is about to start a long-term decline. With labour more scarce, they argue, workers can negotiate for higher wages, which will translate into inflation [6].

The reality is much more intricate, contributing to the ongoing debates, with government policies playing a pivotal role in addressing issues through reforms. However, what's undeniable is the importance of factoring in demographics when making investment decisions.

3) Netflix goes Raw

Starting next year, Netflix plans to deliver three hours of live wrestling each week. It marks its entry into the live "sports" arena, carefully categorising it as "Sports Entertainment" to align with its existing content. They reportedly invested $5 billion for a 10-year exclusive rights deal for Raw in the United States, Canada, Latin America and certain international markets [7].

Through this agreement, Netflix seeks to attract millions of dedicated WWE fans, giving a lift to its growing advertising-supported model. While the company has experimented with live events in the past year, such as a live comedy special and a golf match, this marks its first significant long-term commitment.

Companies like Apple, Google and Amazon have shown a keen interest in increasing viewership for their streaming subscription services and actively engaged in talks to secure media rights from major sports entities such as the National Football League, Major League Baseball, and Formula One racing.

Their enthusiasm is exciting for sports leagues but unnerving for media companies, who are apprehensive about competing with rivals who amass substantial funds from dominating other industries. In 2021, sports dominated television, with 95 out of the top 100 most-watched programs [8].

Ironically, Netflix CEO Reed Hastings had once dismissed live sports and news, asserting that they lacked replay value [9] – a sentiment echoed by others in the industry. In 2025, we'll find out about the accuracy of that prediction.

Notices

Please remember, investing should be viewed as longer term. Your capital is at risk — the value of investments can go up and down, and you may get back less than you put in.

References

[2] https://fred.stlouisfed.org/series/FEDFUNDS

[3] https://www.statista.com/statistics/1058454/yield-curve-usa/

[4] https://www.spglobal.com/spdji/en/indices/equity/sp-500-equal-weight-index/#overview

[5] https://www.federalreserve.gov/econresdata/feds/2016/files/2016080pap.pdf

[8] https://www.nytimes.com/2022/07/24/technology/sports-streaming-rights.html

[9] https://www.engadget.com/2018-03-07-netflix-ceo-reed-hastings-live-tv-disney-marvel.html